Let's get critical

Can technology save mining?

A lot of clever people said a lot of clever things last year about the importance of owning manufacturing for US/European economic and military resilience.

It was like the talking heads had a collective Damascene realisation that China was no longer “copying” Western innovation, and was actually making all the best stuff, way cheaper and way faster than anyone else could, and that this would be really rather bad if we ended up in direct conflict, say, over Taiwan.

While the importance of this has in no way abated, over the course of 2025 this narrative began to shift a layer deeper - to focus on critical minerals supply. This is an area I find particularly fascinating, believing that the supply of critical minerals is even more important to economic and military sovereignty than owning the factories.

Why? Well, everything important to the modern economy is absolutely full of critical minerals. Our whole economy is downstream of these elements, and it doesn’t matter how many factories you have if you don’t own the supply of stuff to fuel them.

Not only are these magical materials axiomatic to the modern world, but it turns out (much like most manufacturing) that we largely don’t own their supply or processing in the West, yet our growth in demand is far outstripping our ability to dig them out of the ground.

Technology is going to play a major role here - the following is my attempt to dig into some ideas around how.

They’re called critical minerals for a reason

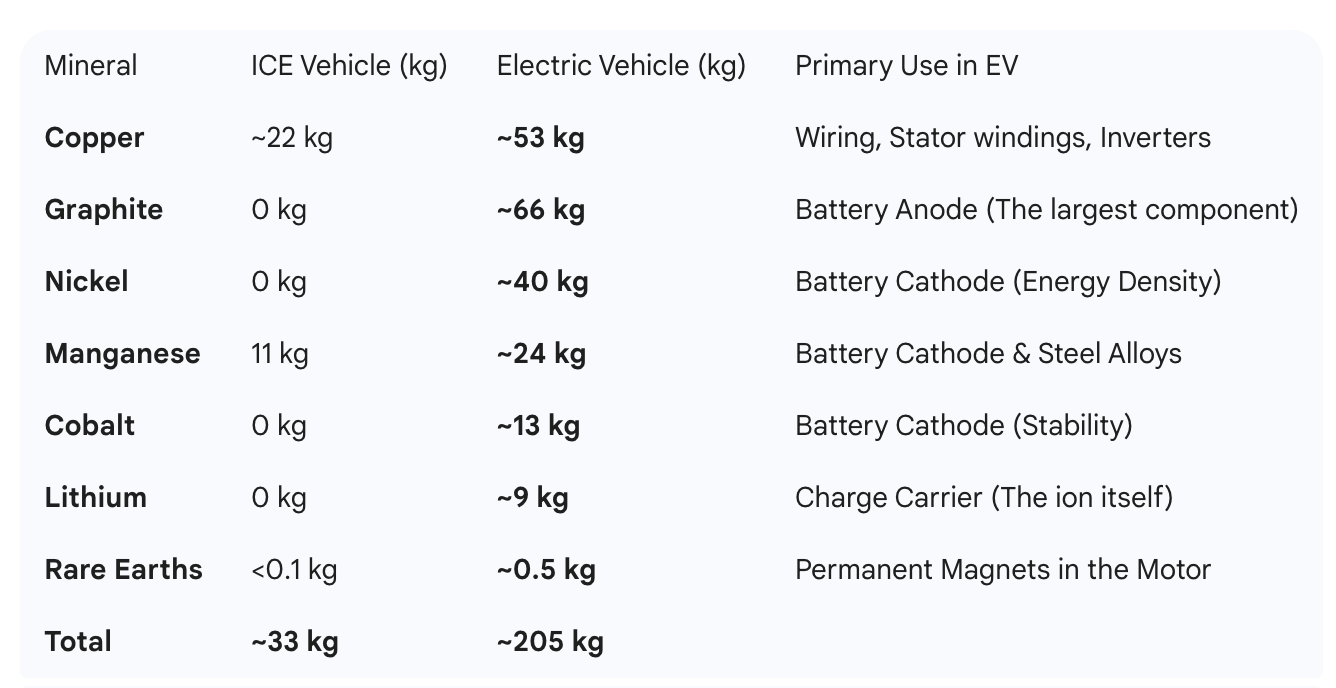

For the uninitiated, critical minerals is an umbrella term for those minerals considered to have a role in a country’s strategically important economic sectors - changing by nation but generally including copper, lithium, nickel, gold, graphite, cobalt, manganese and the rare earth metals (17 heavy metals found throughout the earth’s crust).

Global demand for these elements has been increasing since societies industrialised, rising steadily (~2-3% YoY) in the 20th century. Around the turn of the century this rapidly accelerated, driven by the rise of China then the push towards electrification and green technologies, with growth rates looking more like 5-15% on average since the turn of the millennium, with specific materials (e.g. lithium 25-30%, cobalt 10-15%) growing considerably faster.

This is because these minerals are central to just about everything important in an electrified society - batteries, magnets, motors, chips, advanced/power electronics, fibre optics, cables, touchscreens etc. For example, your average electric vehicle looks like this:

Given that an EV is, as of 2026, in many ways a massive smartphone with wheels - these same laws scale down to microchip level and up to massive electric devices like wind turbines or industrial batteries. Everything we use today that involves an electronic component, from a printer to a fighter jet, is stock full of critical minerals.

And this historic growth is only accelerating. Lithium demand is forecast to triple by 2040 relative to current levels, driven primarily by the ubiquity of lithium-ion batteries in EVs and stationary devices. Cobalt demand is projected to more than double by 2040, driven by its role in stabilising battery cathodes, while copper (literally known as the “metal of electrification”) demand is expected to add 50% by 2040 - with a structural deficit of 12 million tonnes predicted by 2035. Nickel & rare earths have similar predicted trajectories, with significant pressure on supply chains for high-performance magnets and high-nickel battery chemistries.

Yet the fundamental challenge here is that we currently can’t match supply to meet this exploding demand.

It turns out mining is really quite difficult

This comes down to a number of reasons, but the main ones is that developing a new mine is very uncertain and takes absolutely ages.

The average time from discovery to first production for a new mine has ballooned to ~18 years from ~12 in the 2000s. This delay is rarely caused by the construction of the mine - instead its a combination of deposits being buried deeper under the ground (the easy, near surface finds have all been discovered in a well trodden world), the explosion of bureaucracy and permitting needs in many nations (e.g. the US average time to mine is now more like 30 years), and the financing challenges for the smaller (Junior) miners who are often those to discover new seams but get stuck raising capital with which to fund drilling.

Given the lag, the mines required to meet 2035 demand should have been discovered in 2017. In large part they were not.

Alongside this, the quality of available ore is degrading worldwide. For copper, average head grades (avg. concentration of valuable metal or mineral in the ore as it’s delivered from the mine to the processing mill) in Chile have fallen from >1.5% to <0.6% over the last two decades. Lower grades require moving more earth to extract the same amount of metal, increasing energy costs, timelines and capex even further.

Zero sum diplomacy

And this is before one considers the concentration of supply chains and the geopolitical relevance of these elements. The supply chain for many critical minerals is dangerously concentrated, and not in nations necessarily friendly to US or European interests.

While around 75% of raw lithium supply comes from Australia and Chile, China owns 60-70% of the processing. The picture is similar for cobalt - while ~75% of of supply from the DRC, China dominates 70% of processing. And the same again with rare earths - more or less 90% Chinese owned. Copper? You guessed it - China owns just 8% of mine output, but over 45% of refined production. So while supply may be more distributed, when it comes to refining, there’s really only one buyer of relevance.

This is also complicated and often nasty business - developing countries with unstable regimes, unclear/corrupt regulatory frameworks, varying geopolitical alignments and interests, labour forces at times employing quasi slave labour, and entrenched Chinese economic power wherever you look.

This is what the EU and US have finally woken up to in recent years. The 2022 US Inflation Reduction Act offered benefits for domestic production, while in 2024 the EU Critical Raw Materials Act mandated sourcing 10% from EU extraction, 40% from EU processing, and 25% from EU recycling, while limiting single-country import dependency to 65% for any raw material.

However it was in 2025 these bureaucratic conversations really hit the mainstream, in large part driven by President Trump’s return to the White House. In April and October last year China imposed hefty rare earth export limits as a response to US tariffs, and the Trump administration has subsequently very publicly prioritised non-Chinese critical minerals deals and even taken direct stakes in critical minerals producers to shore up supply.

Viewed through this lens, many of the US’s more dramatic actions and proclamations (e.g. striking Venezuela, threatening Cuba/Greenland/Mexico, or forcing Ukraine into a minerals deal in exchange for aid) begin to reveal an underlying pattern. Per the FT:

Given that mining directly accounts for 1-1.5% of Global GDP (rising to 5-7% when bundled with oil, gas and coal), and the electrification wave shows no signs of slowing down, this geopolitical relevance is only going to grow in coming years.

It is within this context that technology comes into play. Mining has not traditionally been viewed as start-up friendly, being hamstrung by regulation, geographically fragmented, dangerous and about as “analogue” as a sector can get.

However, it is also legacy, oligopolistic and largely resistant to innovation - three things technology companies have been licking their lips at since long before Bezos declared “your margin is my opportunity”. This, combined with the start-up shift towards bigger, bolder hardware-driven bets in recent years has gradually cracked this sleeping giant of a sector open for innovation.

Large models applied to resource discovery

The first (and arguably most important) area of value creation is in optimising the mine discovery and selection process.

Traditionally, identification and selection is done by expert geologists who combine large amounts of topographical data and well established heuristics (e.g. X mineral often occurs alongside Y land formation) with walking prospective sites, taking soil samples, and conducting various surveys (e.g. seismic, gravity).

While based on deep and broad expertise, this approach is human-led, time consuming, manual and limited by teams’ capacity to interpret data. The industry rule suggests around 1/1000 (0.1%) sites make it from initial identification to a revenue generating site - an awful, and time consuming ratio.

Machine learning and agentic solutions are particularly useful here - where humans act both as APIs (transferring data from one point to another) and pattern matchers in large datasets. It is no surprise therefore that a host of companies have emerged trying these approaches but for mine discovery.

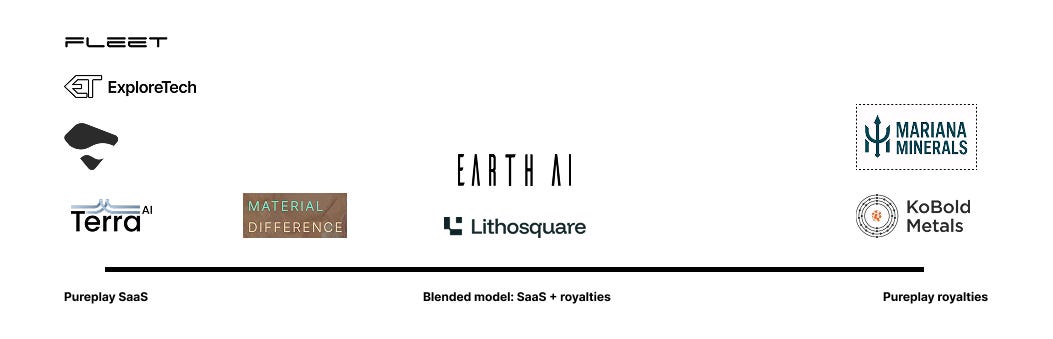

These start-ups and scale-ups exist on a continuum from pure-play software providers (building software tools for Juniors/mid-tiers/Majors to pay for on a recurring basis) through to companies attempting to become full stack mining firms themselves.

On the pure software end, Terra AI and ExploreTech both combine proprietary models and geologist expertise to provide mining discovery companies with insights to better identify and optimise drill sites, similar to UK based new entrant Material Difference who use novel explainable models to optimise site identification and selection - currently as a service to mid-tier miners.

Fleet Space Technologies take a space-based approach employing micro-satellites and proprietary models to aid mineral discovery, while Germany-based Deep Earth is mapping the subsurface world to build a broader 3D picture of the underground for multiple industries. These approaches all focus on software revenues - potentially remunerative as mid-tiers / Majors could easily pay multiple million dollar contract sizes, but equally beholden to powerful, concentrated buyers (~250 mid tiers / ~50 majors controlling 60-70% of the market) and the whims of a slow moving sector.

Where the opportunity gets colossal is when technology companies look to shoulder the risk and temporal uncertainty themselves, leveraging tech to optimise the discovery and operations, but capturing royalties from the output of the mines in place of software revenues.

The household name and first real mover in this space is KoBold Metals, a Breakthrough Energy backed “Google Maps for the Earth’s crust” claiming to have ingested millions of data points into large models to correlate broad variables and optimise mine discovery. KoBald was one of the first tech companies to shift from serving third parties to taking on the risk themselves - looking to replicate the work of Junior miners but in a tech-enabled, hyper efficient manner.

It is of note that they transitioned from being a broader exploration company into owning a single Zambian copper mine - due to the massive royalties (+$100m) on offer once the right site has been selected, but also likely due to the slow moving and high uncertainty nature of marginal site identification. As of January ‘26, they appear to be exploring a second site in the DRC.

a16z backed Mariana Minerals have built on this approach, looking to develop a “mine in a box” solution to rapidly deploy new mines across the globe, capturing the site output in the process. Their focus is on post discovery implementation, buying sites or permits off cash strapped discovery companies. Per a16z’s blog post “Mariana is full-stack. It designs, permits, finances, commissions, and operates. It pours the concrete. It operates the haul truck. Where incumbents take twelve years to get a single lithium project into production, Mariana has set a target that sounds like heresy: 10 mineral projects in 10 years.”

Also in this space are Australian Earth AI that began as a pure-play software provider and moved into a verticalized offering, claiming an astonishing 75% identification hit rate. French start-up Lithosquare is building a multi-agent full stack discovery company, combining the initial ML-driven discovery work with workflows designed to optimise the whole prospecting process, while US-based VerAI is going after the same pie with their own data-driven approach.

While potentially longer to revenues, the upside for these royalty-driven discovery companies is uncapped. The challenge will be whether they can materially alter the structure of the mining sector - either prospecting a sufficiently large number of sites so as to hedge their bets across dozens of projects, or achieving a suitably high level of accuracy to enable “one shot one kill” approaches to site identification.

The fundamental tension is this time to revenues vs. risk. Majors (e.g. Rio Tinto, BHP) have dozens of projects and massive balance sheets, enabling them to trade at 6-20x P:E multiples (share price / earnings per share) and ride out failed projects or slow timelines. However the smaller discovery companies (Juniors) are highly leveraged into single exploration projects, trading at very low P:NAV ratios (i.e. enterprise value vs. the potential value of the ore discoveries) as a result of this concentration and the awful, slow throughput of initial site identification to profitable mine.

So, if novel, vertically integrated technology players can improve this 0.1% hit rate / 18Y lag in a meaningful manner - through tightening the funnel of initial sites, optimising drilling, or getting mines up and running more quickly (and so increasing no. of bets) - they can act like Majors at the scale of Juniors - unlocking massive revenues and accompanying valuation multiples accordingly.

This will take a level of ambition and operational brilliance akin to tech enabled drug discovery, neoprimes in defence or challenger space exploration companies. Bringing best in class machine learning talent together with legacy geology know-how, shortening time to revenues and site discovery uncertainty, and building expertise and network in a difficult, dangerous sector, all while likely stepping on the toes of the mining Majors - organisations it wouldn’t generally be advised to wilfully irritate.

I believe the technology opportunity here is largely untapped and hugely exciting. Evidence from legacy miners suggests they are very early in their tech adoption journey, and will no doubt struggle to incorporate many of these innovations in any meaningful way. Put simply - there’s a +$1tn industry ripe for disruption.

To be continued

Part two coming shortly - going deeper into net new ore sources, solving the mineral processing concentration challenge, mine management, teleoperation, automation and more. Have I missed anything? Let me know.

I’m Max - I write sporadically about things that interest me, often centred around technology and how it affects our lives, while investing in start-ups via Kindred Capital and Anti Ordinary. Loved it, hated it? Neither? Tell me, or just binge my content @ maxbray.xyz

The way out —> heliogenesis.io